One of the most common questions we get asked is “Should I pay off my mortgage early?” In our low-interest-rate environment, most people have better options, including paying down high-interest debt and investing for retirement. While paying off a mortgage early will save you money on interest, you need to examine your whole financial picture before putting your hard-earned excess cash to work.

A home with or without a mortgage is worth the same, so the only financial benefit to paying off a mortgage early is to save on interest. However, you also need to ask, “Does it actually cost me to save on interest?”

A key consideration for paying down debt is comparing “interest saved” versus “interest earned.” In most circumstances, it is better to allocate excess cash to high-interest debt, such as credit cards, or invest in your retirement. When making any financial decision, take some time to do the math and compare scenarios.

The Interest Rate Impact

Rather than pay extra on their mortgage, most people should apply the extra cash to things with higher expected returns or interest.

Interest rates are near historic lows and have been for some time. While your mortgage rate will depend on several factors, such as your credit score, rates generally follow the 10-year Treasury yield. It has been common to acquire a 4% interest (often less) 30-year mortgage over the last decade.

Meanwhile, the long-term stock market has averaged nearly 10% per year, and the long-term bond market has averaged between 5 and 6%. Credit card debt can be as high as 18%, and the long-term inflation rate is near 3%.

Compounding vs. Amortizing

Another major factor to consider is what type of interest you are paying off. The distinction here is between the function of compounding and amortizing.

Compounding is when interest is added back into the principal on a schedule, which in turn earns interest itself, growing exponentially over time. Compounding schedules can be yearly, quarterly, monthly, even daily!

Credit cards and student loans use compounding interest. As interest accumulates, it also carries interest, which is why some people have such trouble paying off those types of loans.

Investing returns are also compounding. Dividends, interest, and growth through retained earnings are reinvested, and those accumulations also grow earnings.

Amortizing is spreading out interest at set intervals over the life a loan. Virtually all mortgages use amortization, where each payment has a set different amount of principal and interest. In the beginning, most of the mortgage payment is applied to interest. Over time, interest payments gradually decrease to zero when the loan is paid off.

In other words, when paying down an amortized loan, such as a mortgage, you “save” less with each payment made; the rest is applied to principal. Paying extra principal saves future interest, which has a compounding effect, but the loan interest is still not compounding.

Let’s look at some examples using a 4% rate and $100,000 amount to compare compounding in an investment account with amortizing interest in a loan. A $100,000 loan with a 4% interest rate amortized over 30 years would have a total interest cost of $71,869. A lump sum of $100,000 in an investment that is earning 4% compounding interest over the same 30 years would have $231,349 in earned interest!

Now instead of a lump sum of $100,000, let’s say we break it up into equal monthly contributions over 30 years to equal $100,000. That would be equal contributions of $277.78 per month for 30 years. Thirty years of monthly $277.78 contributions compounded at 4% would earn $93,434.

Amortized interest loan: $100,000, 30 years at 4% = $71,869 interest cost

Compounding interest earned:

Lump contribution of $100,000, 30 years at 4% = $231,349 interest earned

Monthly contribution of $277.78, 30 years at 4% = $93,434 interest earned

These examples show when given a choice, you want your money to earn money and grow through compounding, such as investing.

Both compounding examples contributed $100,000 into an investment, but the lump amount earned 247% more over the same period due to the time value of compounding.

It is possible to earn more through compounding with a lower rate than paying off a higher amortized rate—it just depends on the spread between rates and time period.

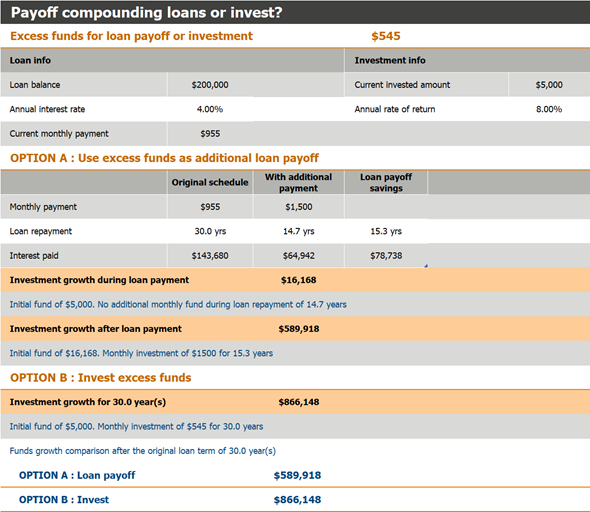

Let’s look at a real-world example. A 30-year-old newly married couple has decided to purchase a home. The mortgage on the house is $200,000 for 30 years at 4%. For the most part, they have waited to invest up to this point and have only $5,000 split between their 401(k)s at work, earning an average of 8% per year.

The principal and interest on the mortgage are $955 per month, but the couple has a total of $1,500 per month they would like to apply to their “long-term goals.” They are interested in paying off the mortgage in half the time, then taking the full $1,500 to invest in their retirement. They feel that being “debt-free” will put them ahead and better prepare them for retirement.

Let’s do the math and see whether it is better to apply the extra $545 to the mortgage and then invest all $1,500 per month toward retirement going forward. Alternatively, the couple could just pay the regular mortgage payment over 30 years and invest the remaining $545 each month.

Either way, exactly $1,500 is spent per month for 30 years between the mortgage and investment. The loan is 4%, and the average investment earnings are 8%.

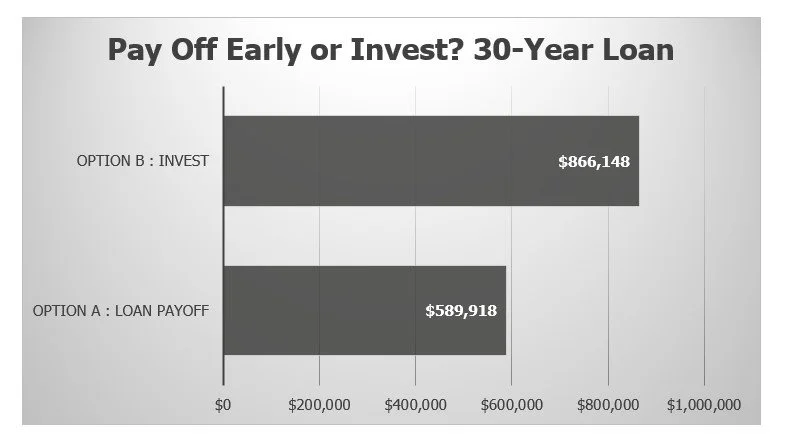

The difference in results with the same monthly out-of-pocket cash flow is dramatic. Option A takes the full $1,500 per month to pay off the mortgage early—i.e., they wait to invest until the mortgage is paid off. After the loan is paid off in 14.7 years, that total of $1,500 is then applied to the couple’s retirement investment every month. While the couple saves $78,738 in interest, they LOSE $276,230 in growth!

Option B, paying the minimum mortgage payment and allocating the additional $545 per month to their retirement investment, leaves the couple with almost 50% more money with the same out-of-pocket cash flow. The chart below shows the breakdown.

The story does not end there. Remember, the investment provides compounding returns. That difference of $276,230 in earnings grows on itself. Let’s continue with the example and assume the couple is now 60 years old and will continue paying $1,500 toward their retirement for five more years until age 65. You can see below that Option B vastly outperforms Option A and starts to grow at an even faster rate due to more money being compounded.

Again, the chart illustrates how powerful the time factor is in compounding.

The chart below illustrates how dramatic disciplined, systematic investing can be. All examples invest $6,000 annually, the current maximum amount allowed for an individual retirement account (IRA), and assume an annual growth rate of 8%.

Each line illustrates an investor who started out at $0 at their listed age and continued to invest $6,000 per year until 65, except for the yellow line. The yellow line started investing at age 25, stopped at 35, and never added another $1 of new investment. This person invested one-third as much as the person who waited until 35 to start investing and ended with over $250,000 more in retirement.

This example illustrates how time is such a big factor in compounding returns. It also shows that someone can have substantial retirement savings using relatively small monthly contributions. Yes, most people of even modest income can and should be millionaires by retirement if they start planning early and strategically.

All the above examples illustrate how strategically applying excess cash flow can have massive effects on your overall wealth. As the Chinese proverb says, “The best time to plant a tree was 20 years ago. The second-best time is now.” It is never too late to start seeking compounding returns, whether investing in stocks or bonds or paying down high-interest debt.

Your Answer Is Unique to You

The answer to the question “Should I pay off my mortgage early?” is NO for most people. However, to show compounding returns versus paying off debt in isolation, the above examples intentionally left out numerous complexities most people experience.

When determining your action plan for using excess cash flow, you should have a comprehensive financial plan that analyzes how different investment strategies, investment accounts, retirement accounts, inflation, insurance, changes in earned income, employment benefits, pre-tax vs. Roth IRAs, Social Security income, pension income, current and future taxes, and more can best help you achieve your goals.

Further, there are important personal and emotional factors that need to be considered. For some, the opportunity cost of paying off low-interest debt is worth the trade-off of earning more savings. For others, early retirement is more valuable than additional earnings. These personal decisions are easier to make when you have a clear picture of the outcome of your choices.

The most important factor in determining what to do with excess cash is making wise decisions that connect your money to your goals and values. If you would like to speak with a financial planner about the action steps you should take, schedule a complimentary 30-minute discovery call with one of our CERTIFIED FINANCIAL PLANNER™ (CFP®) professionals.